- What is Inflation?

Inflation

is the rate at which the general level of prices for goods and services is

rising and, consequently, the purchasing power of currency is

falling. Central banks attempt to limit inflation, and

avoid deflation, in order to keep the economy running smoothly. In

economics, inflation is a rise in the general level of prices of

goods and services in an economy over a period of time. When the general price

level rises, each unit of currency buys fewer goods and services.

Because the

term inflation is such a generic term used in many contexts, there is

no commonly accepted definition of inflation, nor is there a common

agreement on what constitutes acceptable levels of inflation, bad inflation, or

hyperinflation.

Because the

term inflation is such a generic term used in many contexts, there is

no commonly accepted definition of inflation, nor is there a common

agreement on what constitutes acceptable levels of inflation, bad inflation, or

hyperinflation.

Generally it can be said

that inflation is a measure of a general increase of the price level in an

economy, as represented typically by an inclusive price index, such as the

Consumer Price Index (CPI). The term indicates many individual prices rising

together rather than one or two isolated prices, such as the price of gasoline

in an otherwise calm price environment.

- Some Types of Inflation:

When the rise in prices is very low

like that of a snail or creeper, is called Creeping Inflation. Running

inflation has inflation rate between 8-10 %. A sense of urgency needs

to be shown in controlling the running inflation. Hyper

Inflation, Latin American countries like Argentina and Brazil had

inflation rates of 50 to 700 percent per year in the between 1970 and 1980. Many

developed and industrialized countries like Italy and Japan still do. Pricing

Power administered price inflation. When the business houses and

industries decide to increase the price of their respective goods and services

to increase their profit margins.

- Causes of Inflation:

Historically,

a great deal of economic literature was concerned with the question of what

causes inflation and what effect it has. There were different schools of

thought as to the causes of inflation. Most can be divided into two broad

areas: quality theories of inflation and quantity theories of inflation. The

quality theory of inflation rests on the expectation of a seller accepting

currency to be able to exchange that currency at a later time for goods that

are desirable as a buyer. The quantity theory of inflation rests on the

quantity equation of money that relates the money supply, its velocity and the

nominal values of exchanges. Adam

Smith and David Hume proposed a quantity theory of inflation for

money, and a quality theory of inflation for production.

Keynesian View:

Keynesian economics proposes

that changes in money supply do not directly affect prices, and that visible

inflation is the result of pressures in the economy expressing themselves in

prices.

There are three major types of

inflation, as part of what Robert J. Gordon calls the "triangle

model”

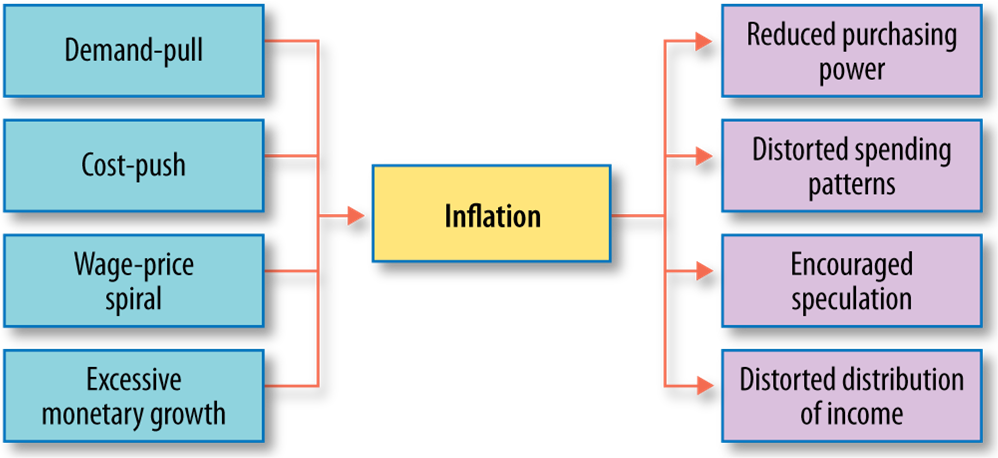

- Demand-pull inflation is caused by increases in aggregate demand due to increased private and government spending, etc. Demand inflation encourages economic growth since the excess demand and favorable market conditions will stimulate investment and expansion.

- Cost-push inflation, also called "supply shock inflation," is caused by a drop in aggregate supply (potential output). This may be due to natural disasters, or increased prices of inputs. For example, a sudden decrease in the supply of oil, leading to increased oil prices, can cause cost-push inflation. Producers for whom oil is a part of their costs could then pass this on to consumers in the form of increased prices. Another example stems from unexpectedly high Insured losses, either legitimate (catastrophes) or fraudulent (which might be particularly prevalent in times of recession).

- Built-in inflation is induced by adaptive expectations, and is often linked to the "price/wage spiral". It involves workers trying to keep their wages up with prices (above the rate of inflation), and firms passing these higher labor costs on to their customers as higher prices, leading to a 'vicious circle'. Built-in inflation reflects events in the past, and so might be seen as hangover inflation.

Demand-pull

theory states that inflation accelerates when aggregate

demand increases beyond the ability of the economy to produce

(its potential output). Hence, any factor that increases aggregate demand

can cause inflation. However, in the long run, aggregate demand can be

held above productive capacity only by increasing the quantity of money in

circulation faster than the real growth rate of the economy. Another (although

much less common) cause can be a rapid decline in the demand for

money, as happened in Europe during the Black Death, or in

the Japanese occupied territories just before the defeat of Japan in

1945.

The

effect of money on inflation is most obvious when governments finance spending

in a crisis, such as a civil war, by printing money excessively. This sometimes

leads to hyperinflation, a condition where prices can double in a month or

less. Money supply is also thought to play a major role in determining moderate

levels of inflation, although there are differences of opinion on how important

it is. For example, Monetarist economists believe that the link is

very strong; Keynesian economists, by contrast, typically emphasize the role

of aggregate demand in the economy rather than the money supply in

determining inflation. That is, for Keynesians, the money supply is only one

determinant of aggregate demand.

Some

Keynesian economists also disagree with the notion that central banks fully

control the money supply, arguing that central banks have little control, since

the money supply adapts to the demand for bank credit issued by commercial

banks. This is known as the theory of endogenous money, and has been

advocated strongly by post-Keynesians as far back as the 1960s. It

has today become a central focus of Taylor rule advocates. This

position is not universally accepted – banks create money by making loans, but

the aggregate volume of these loans diminishes as real interest rates increase.

Thus, central banks can influence the money supply by making money cheaper or

more expensive, thus increasing or decreasing its production.

Some

Keynesian economists also disagree with the notion that central banks fully

control the money supply, arguing that central banks have little control, since

the money supply adapts to the demand for bank credit issued by commercial

banks. This is known as the theory of endogenous money, and has been

advocated strongly by post-Keynesians as far back as the 1960s. It

has today become a central focus of Taylor rule advocates. This

position is not universally accepted – banks create money by making loans, but

the aggregate volume of these loans diminishes as real interest rates increase.

Thus, central banks can influence the money supply by making money cheaper or

more expensive, thus increasing or decreasing its production.

A

fundamental concept in inflation analysis is the relationship between inflation

and unemployment, called the Phillips curve. This model suggests that

there is a trade-off between price stability and employment.

Therefore, some level of inflation could be considered desirable in order to

minimize unemployment. The Phillips curve model described the U.S. experience

well in the 1960s but failed to describe the combination of rising inflation

and economic stagnation (sometimes referred to as stagflation) experienced

in the 1970s.

Thus,

modern macroeconomics describes inflation using a Phillips curve

that shifts (so the trade-off between inflation and unemployment

changes) because of such matters as supply shocks and inflation becoming built

into the normal workings of the economy. The former refers to such events as

the oil shocks of the 1970s, while the latter refers to the price/wage spiral and inflationary

expectations implying that the economy "normally" suffers from

inflation. Thus, the Phillips curve represents only the demand-pull component

of the triangle model.

Another

concept of note is the potential output (sometimes called the

"natural gross domestic product"), a level of GDP, where the economy

is at its optimal level of production given institutional and natural

constraints. (This level of output corresponds to the Non-Accelerating

Inflation Rate of Unemployment, NAIRU, or the "natural" rate of

unemployment or the full-employment unemployment rate.) If GDP exceeds its

potential (and unemployment is below the NAIRU), the theory says that inflation

will accelerate as suppliers increase their prices and built-in

inflation worsens. If GDP falls below its potential level (and unemployment is

above the NAIRU), inflation will decelerate as suppliers attempt to

fill excess capacity, cutting prices and undermining built-in inflation.

Another

concept of note is the potential output (sometimes called the

"natural gross domestic product"), a level of GDP, where the economy

is at its optimal level of production given institutional and natural

constraints. (This level of output corresponds to the Non-Accelerating

Inflation Rate of Unemployment, NAIRU, or the "natural" rate of

unemployment or the full-employment unemployment rate.) If GDP exceeds its

potential (and unemployment is below the NAIRU), the theory says that inflation

will accelerate as suppliers increase their prices and built-in

inflation worsens. If GDP falls below its potential level (and unemployment is

above the NAIRU), inflation will decelerate as suppliers attempt to

fill excess capacity, cutting prices and undermining built-in inflation.

However,

one problem with this theory for policy-making purposes is that the exact level

of potential output (and of the NAIRU) is generally unknown and tends to change

over time. Inflation also seems to act in an asymmetric way, rising more

quickly than it falls. Worse, it can change because of policy: for example,

high unemployment under British Prime Minister Margaret

Thatcher might have led to a rise in the NAIRU (and a fall in potential)

because many of the unemployed found themselves as structurally

unemployed, unable to find jobs that fit their skills. A rise in structural

unemployment implies that a smaller percentage of the labor force can find jobs

at the NAIRU, where the economy avoids crossing the threshold into the realm of

accelerating inflation.

Unemployment:

A connection

between inflation and unemployment has been drawn since the emergence of large

scale unemployment in the 19th century, and connections continue to be drawn

today. However, the unemployment rate generally only affects

inflation in the short-term but not the long-term. In the long term, the velocity

of money supply measures such as the MZM ("Money Zero Maturity,"

representing cash and equivalent demand deposits) velocity is far more

predictive of inflation than low unemployment.

During the Great Depression, the classical theory

attributed mass unemployment to high and rigid real wages.

To Keynes, the

determination of wages was more complicated. First, he argued that it is not real but nominal wages that are set in negotiations

between employers and workers, as opposed to a barter relationship. Second, nominal wage

cuts would be difficult to put into effect because of laws and wage contracts.

Even classical economists admitted that these exist; unlike Keynes, they

advocated abolishing minimum wages, unions, and long-term contracts, increasing labour market flexibility. However, to

Keynes, people will resist nominal wage reductions, even without unions, until

they see other wages falling and a general fall of prices.

Keynes rejected the

idea that cutting wages would cure recessions. He examined the explanations for

this idea and found them all faulty. He also considered the most likely

consequences of cutting wages in recessions, under various different

circumstances. He concluded that such wage cutting would be more likely to make

recessions worse rather than better.

Further, if wages

and prices were falling, people would start to expect them to fall. This could

make the economy spiral downward as those who had money would simply wait as falling

prices made it more valuable – rather than spending. As Irving Fisher argued in 1933, in his Debt-Deflation

Theory of Great Depressions, deflation (falling prices) can make a depression

deeper as falling prices and wages made pre-existing nominal debts more

valuable in real terms.

- Inflation Thresholds:

{kind=link}

Table 1 shows somewhat

arbitrary thresholds. Other economists would have thresholds a little more

strident than this, yet others a little looser. When you look at Table 1

it is clear that a nominal amount of inflation, typically less than 3%, is

accepted and might even be good for the economy.1 But any sustained level above

2.5% or 3% will be seen as a potential problem, and the higher the rate, the

more serious and dangerous the problem. Part of the reason for this is because

once inflation moves up into the high single-digit range and then double-digit

range, it begins to self-compound into a higher rate. In other words, once it

reaches a certain rate, it sets in motion a series of forces that tend to move

it automatically to a higher rate (explained later). More bluntly, a 12%

inflation will automatically become a 15% inflation and then a 20% inflation if

not dealt with using severe and relentless anti-inflation policies. Once

inflation moves above the 20% range, lessons from history tells us that the

tendency to self-compound is so great that the inflation becomes explosive and

potentially ruinous to an economy.

Table 1 shows somewhat

arbitrary thresholds. Other economists would have thresholds a little more

strident than this, yet others a little looser. When you look at Table 1

it is clear that a nominal amount of inflation, typically less than 3%, is

accepted and might even be good for the economy.1 But any sustained level above

2.5% or 3% will be seen as a potential problem, and the higher the rate, the

more serious and dangerous the problem. Part of the reason for this is because

once inflation moves up into the high single-digit range and then double-digit

range, it begins to self-compound into a higher rate. In other words, once it

reaches a certain rate, it sets in motion a series of forces that tend to move

it automatically to a higher rate (explained later). More bluntly, a 12%

inflation will automatically become a 15% inflation and then a 20% inflation if

not dealt with using severe and relentless anti-inflation policies. Once

inflation moves above the 20% range, lessons from history tells us that the

tendency to self-compound is so great that the inflation becomes explosive and

potentially ruinous to an economy.

- Controlling Inflation:

Monetary Policy:

Governments and

central banks primarily use monetary policy to control inflation. Central

banks such as the U.S. Federal Reserve increase the interest

rate, slow or stop the growth of the money supply, and reduce the money supply.

Some banks have a symmetrical inflation target while others only

control inflation when it rises above a target, whether express or implied.

Most central banks

are tasked with keeping their inter-bank lending rates at low levels, normally

to a target annual rate of about 2% to 3%, and within a targeted annual

inflation range of about 2% to 6%. Central bankers target a low inflation rate

because they believe deflation endangers the economy.

Most central banks

are tasked with keeping their inter-bank lending rates at low levels, normally

to a target annual rate of about 2% to 3%, and within a targeted annual

inflation range of about 2% to 6%. Central bankers target a low inflation rate

because they believe deflation endangers the economy.

Higher interest

rates reduce the amount of money because fewer people seek loans, and loans are

usually made with new money. When banks make loans, they usually first create

new money, then lend it. A central bank usually creates money lent to a

national government. Therefore, when a person pays back a loan, the bank

destroys the money and the quantity of money falls. In the early 1980s, when

the federal funds rate exceeded 15 percent, the quantity

of Federal Reserve dollars fell 8.1 percent, from $8.6 trillion down

to $7.9 trillion.

Monetarists

emphasize a steady growth rate of money and use monetary policy to

control inflation by increasing interest rates and slowing the rise in the

money supply. Keynesians emphasize reducing aggregate demand during

economic expansions and increasing demand during recessions to keep inflation

stable. Control of aggregate demand can be achieved using both monetary policy

and fiscal policy (increased taxation or reduced government spending

to reduce demand).

Fixed Exchange Rates:

Under

a fixed exchange rate currency regime, a country's currency is tied in value to

another single currency or to a basket of other currencies (or sometimes to

another measure of value, such as gold). A fixed exchange rate is usually used

to stabilize the value of a currency, vis-a-vis the currency it is pegged to.

It can also be used as a means to control inflation. However, as the value of

the reference currency rises and falls, so does the currency pegged to it. This

essentially means that the inflation rate in the fixed exchange rate country is

determined by the inflation rate of the country the currency is pegged to. In

addition, a fixed exchange rate prevents a government from using domestic

monetary policy in order to achieve macroeconomic stability.

Under the Bretton Woods agreement, most countries around the

world had currencies that were fixed to the US dollar. This limited inflation

in those countries, but also exposed them to the danger of speculative

attacks. After the Bretton Woods agreement broke down in the early 1970s,

countries gradually turned to floating exchange rates. However, in the

later part of the 20th century, some countries reverted to a fixed exchange

rate as part of an attempt to control inflation. This policy of using a fixed

exchange rate to control inflation was used in many countries in South America

in the later part of the 20th century (e.g. Argentina (1991–2002),

Bolivia, Brazil, and Chile).

Gold Standard:

The gold standard

is a monetary system in which a region's common media of exchange are paper

notes that are normally freely convertible into pre-set, fixed quantities of

gold. The standard specifies how the gold backing would be implemented,

including the amount of specie per currency unit. The currency itself

has no innate value, but is accepted by traders because it can be

redeemed for the equivalent specie. A U.S. silver certificate, for

example, could be redeemed for an actual piece of silver.

The gold standard

was partially abandoned via the international adoption of the Bretton

Woods System. Under this system all other major currencies were tied at fixed

rates to the dollar, which itself was tied to gold at the rate of $35 per

ounce. The Bretton Woods system broke down in 1971, causing most countries to

switch to fiat money – money backed only by the laws of the country.

The gold standard

was partially abandoned via the international adoption of the Bretton

Woods System. Under this system all other major currencies were tied at fixed

rates to the dollar, which itself was tied to gold at the rate of $35 per

ounce. The Bretton Woods system broke down in 1971, causing most countries to

switch to fiat money – money backed only by the laws of the country.

Under a gold

standard, the long term rate of inflation (or deflation) would be determined by

the growth rate of the supply of gold relative to total output. Critics

argue that this will cause arbitrary fluctuations in the inflation rate, and

that monetary policy would essentially be determined by gold mining.

Wages and Price Control:

Another method

attempted in the past have been wage and price

controls ("incomes policies"). Wage and price controls have been

successful in wartime environments in combination with rationing. However,

their use in other contexts is far more mixed. Notable failures of their use

include the 1972 imposition of wage and price controls by Richard Nixon.

More successful examples include the Prices and Incomes Accord in

Australia and the Wassenaar Agreement in the Netherlands.

Temporary controls

may complement a recession as a way to fight inflation: the

controls make the recession more efficient as a way to fight inflation

(reducing the need to increase unemployment), while the recession prevents the

kinds of distortions that controls cause when demand is high. However, in

general the advice of economists is not to impose price controls but to

liberalize prices by assuming that the economy will adjust and abandon

unprofitable economic activity. The lower activity will place fewer demands on

whatever commodities were driving inflation, whether labor or resources, and

inflation will fall with total economic output. This often produces a severe

recession, as productive capacity is reallocated and is thus often very unpopular

with the people whose livelihoods are destroyed.

Stimulating Economic Growth:

If economic

growth matches the growth of the money supply, inflation should not occur

when all else is equal. A large variety of factors can affect the rate of

both. For example, investment in market production, infrastructure,

education, and preventative health care can all grow an economy in

greater amounts than the investment spending.

Cost-of-living Allowance:

The real

purchasing-power of fixed payments is eroded by inflation unless they are

inflation-adjusted to keep their real values constant. In many countries,

employment contracts, pension benefits, and government entitlements (such as social

security) are tied to a cost-of-living index, typically to the consumer

price index. A cost-of-living allowance (COLA) adjusts

salaries based on changes in a cost-of-living index. It does not control

inflation, but rather seeks to mitigate the consequences of inflation for those

on fixed incomes. Salaries are typically adjusted annually in low inflation

economies. During hyperinflation they are adjusted more often. They may

also be tied to a cost-of-living index that varies by geographic location if

the employee moves.

Annual escalation

clauses in employment contracts can specify retroactive or future percentage

increases in worker pay which are not tied to any index. These negotiated

increases in pay are colloquially referred to as cost-of-living adjustments

("COLAs") or cost-of-living increases because of their similarity to

increases tied to externally determined indexes.

The latest figures of SPI are for 24 April 2014. When

compared to the prices of items in SPI basket from the one week before i.e. 17

April 2014,

Given

the persistent downward trend in inflation over the last ten months, CPI

inflation for the year 2012-13 is forecast-ed to hover around 8.0%. The

availability of food items and any adverse external hike in prices. Seems

unlikely, therefore, the upside risk to inflation for one remainder of FY13 is

minimal. However the revision of any energy tariffs and imposition of taxes may

pose risk to inflation beyond FY13. Food supply at affordable price is the

focal point of food security policy of Pakistan and the four dimensions of food

security also include food availability, food accessibility, food utilization

and food stability which have always been on the high agenda of food policy. It

is hoped that implementations of the policy in letter and spirit will to

further contain the inflation and ensure secure food environment for the

growing population.

- Inflation Trend in Pakistan:

The latest figures of SPI are for 24 April 2014. When

compared to the prices of items in SPI basket from the one week before i.e. 17

April 2014,- 7 items prices have increased while 17 items prices decreased in one week period.

- Following are the figures from “Monthly review on Price Indices” Mar 2014, Base 2007-2008.

- Economic Condition of Pakistan:

High

inflation is contributing to:

- Increasing vulnerability and fall in real income of lower, middle and fixed

income segments of the society.

- Uncertainty

about future scenario of the business environment and instability of the

financial system

- Erosion

of business and investors’ confidence

- Slowing

down of real economic activities

- Investment

- Economic growth

- Employment

Inflation Rate Year-Wise:

Inflation By Consumer Income Group:

Regional Inflation Trend:

Whole Price Index:

Pakistan's and Bangladesh's Inflation Rate:

- Conclusion:

Given

the persistent downward trend in inflation over the last ten months, CPI

inflation for the year 2012-13 is forecast-ed to hover around 8.0%. The

availability of food items and any adverse external hike in prices. Seems

unlikely, therefore, the upside risk to inflation for one remainder of FY13 is

minimal. However the revision of any energy tariffs and imposition of taxes may

pose risk to inflation beyond FY13. Food supply at affordable price is the

focal point of food security policy of Pakistan and the four dimensions of food

security also include food availability, food accessibility, food utilization

and food stability which have always been on the high agenda of food policy. It

is hoped that implementations of the policy in letter and spirit will to

further contain the inflation and ensure secure food environment for the

growing population.

- Some Recommendations:

- Proper taxation system.

- Increase export.

- Increase foreign reserves.

- Control corruption.

- Devaluation of money.

- Produce Electricity.

- Broaden tax collection.